How to Read a Resale Insurance Policy Listing: A Singapore Investor's Guide

A resale insurance policy listing summarises key details like initial investment, yearly premiums, projected maturity value, and estimated return. Learn what each field means and what to review before choosing a policy.

A resale insurance policy listing is a structured table of existing insurance policies available for investors to review and potentially acquire. Each row represents a real, specific policy — with its own insurer, terms, premium schedule, and maturity timeline.

At MAXX CAPITAL, the policy list gives investors a clear first view of available opportunities. It presents the key numbers at a glance and lets you download the full policy document for deeper review before making any decision.

But a policy listing should not be read like a fixed deposit table or a simple product menu. The numbers summarise; they do not replace the review. This guide explains what every field means, how to compare policies correctly, and what to watch out for before choosing.

What Is a Resale Insurance Policy Listing?

A resale insurance policy listing is a table of existing insurance policies that current owners have decided to sell, making them available for investors to take over.

These may include traded endowment policies, whole life policies, annuity policies, or other savings-type insurance policies that may be transferred from the existing policyholder to a new owner through absolute assignment.

The purpose of the listing is to help investors compare available policies in a practical, structured way — so you can quickly identify which policies may fit your budget, time horizon, and return expectations before deciding which ones to review in detail.

However, the list is only the starting point. A resale insurance policy is not a generic product. Each policy must be reviewed on its own terms.

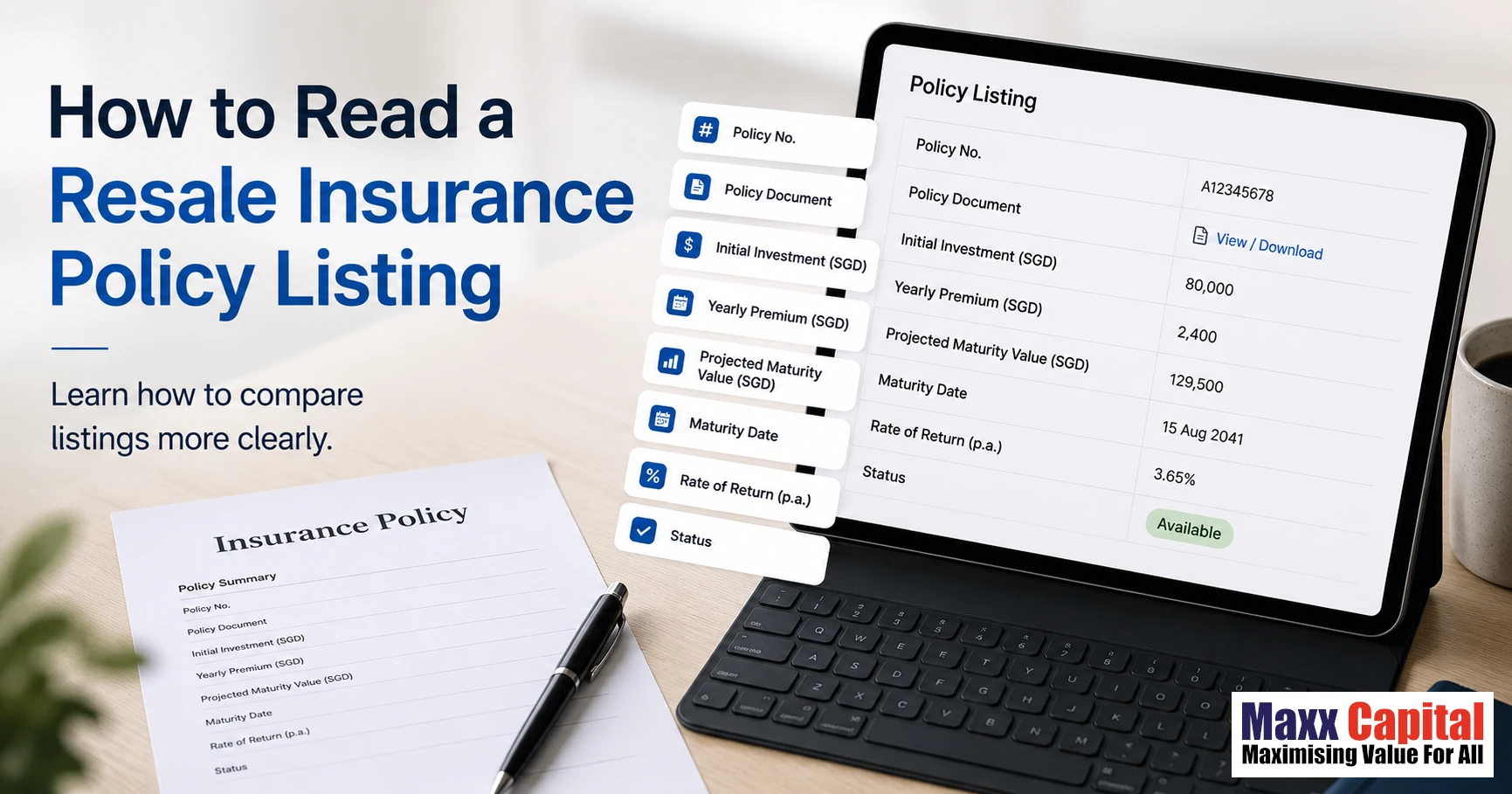

Policy Listing Fields at a Glance

Before diving into each field in detail, here is a summary of what each column in the MAXX CAPITAL policy list represents:

| Field | What It Shows |

|---|---|

| Policy Number | Unique identifier for each listing |

| Policy Document | Downloadable full policy for detailed review |

| Initial Investment | Upfront amount to acquire the policy |

| Yearly Premium | Annual premium still payable after acquisition, if any |

| Projected Maturity Value | Estimated total payout at policy maturity |

| Maturity Date | When the policy is expected to mature |

| Est. Annual Return | Annualised estimated return based on projected figures |

| Status | Whether the policy is currently available |

Each field serves a specific purpose. Understanding them correctly is the difference between a well-informed decision and one based on a single attractive number.

Policy Number

The policy number is the unique identifier for each listing.

Because multiple policies may share similar maturity dates, investment amounts, or return figures, the policy number is what distinguishes one listing from another. When enquiring about a specific policy with MAXX CAPITAL, always reference the policy number to avoid confusion.

It is not an investment decision factor — but it is an important reference point throughout the review and acquisition process.

Policy Document

The policy document is the most important element of any listing.

The table gives you a summary. The document gives you the basis for that summary — including the insurer, policy type, premium schedule, guaranteed values, projected values, maturity terms, and any conditions that affect future payouts.

Before making any investment decision, download and review the policy document. A listing may look compelling based on headline numbers, but those numbers only make sense in the context of the actual policy. This is especially true for resale insurance policies, where each policy has its own specific terms rather than being a standardised product.

At MAXX CAPITAL, every listing on the policy list includes a downloadable policy document for exactly this reason.

Initial Investment

The initial investment is the upfront amount required to acquire the resale policy — what you pay to take ownership of the policy through absolute assignment.

It is typically the first number investors check because it determines whether a policy is within their available capital. However, it should never be read in isolation.

A policy with a lower initial investment may still require significant future premiums, making the total commitment higher than it appears upfront. Conversely, a higher initial investment may come with no or minimal remaining premiums.

The initial investment tells you the cost at entry. It does not tell you the total cost to maturity.

Yearly Premium

The yearly premium is the amount that may still need to be paid each year after you take over the policy to keep it in force.

This is one of the most consequential — and most commonly underestimated — fields in the listing.

Not all resale policies have remaining premiums. Some policies are fully paid up, meaning no further regular payments are required. Others may still have several years of premiums ahead. The difference has a significant impact on:

- Total investment cost — premiums paid over the remaining term add to your total outlay

- Cash flow — ongoing premiums require you to budget for payments beyond the initial acquisition

- Return calculations — the estimated return should reflect total costs, not just the initial investment

Before selecting any policy, confirm whether yearly premiums apply, how much they are, and for how long they continue. A policy that appears affordable at entry may require substantially more capital over its remaining term.

Projected Maturity Value

The projected maturity value is the estimated total payout when the policy reaches its maturity date.

This is an important figure — but the word projected carries real weight.

Many endowment and savings-type policies include both guaranteed and non-guaranteed components:

- Guaranteed portion — stated in the policy contract; the insurer is committed to this amount provided the policy remains in force and conditions are met

- Non-guaranteed portion — may depend on future bonus declarations, participating fund performance, or other insurer decisions; this is a projection, not a commitment

The projected maturity value shown in the listing may include both. If you treat the projected figure as fully guaranteed, you may overestimate the certainty of the outcome.

Before investing, review the policy document and identify:

- How much of the maturity value is guaranteed

- How much is non-guaranteed

- What assumptions underpin the projected figure

This does not make a policy unsuitable. It simply means you should understand what you are committing to.

Maturity Date

The maturity date is when the policy is expected to reach its end of term and pay out.

It defines your investment time horizon, and it is one of the most practical filters when comparing policies. A policy maturing in three years suits a very different investor from one maturing in ten.

Before selecting a policy based on its maturity date, ask yourself:

- Does this timeline fit my financial planning needs?

- Am I comfortable holding this policy until maturity?

- If I need liquidity before maturity, do I have alternative resources?

Resale insurance policies are not designed for short-term trading. They are existing policies with defined remaining terms. Surrendering early after acquiring a policy would defeat the purpose of the investment and is generally not the intended exit strategy.

Choose a maturity date that genuinely fits your time horizon, not just the shortest one available.

Seen a policy that looks interesting? View the full policy list to check current availability and download individual policy documents before going further.

Estimated Annual Return

The estimated annual return is an annualised figure based on the policy's projected maturity value, total investment cost, and remaining term.

It is a useful comparison tool — it translates the raw numbers into a percentage that is easier to benchmark across policies and against other asset classes.

However, because projected maturity values may include non-guaranteed components, the displayed return is also partially based on projections. If the actual maturity payout differs from the projected figure, the actual return will differ too.

Use the estimated return as a comparison guide, not as a guaranteed outcome.

A higher displayed return does not automatically make a policy better. A higher return may come with a longer remaining term, higher future premiums, or a greater reliance on non-guaranteed benefits. A lower return may come with a shorter timeline, fewer obligations, and a higher guaranteed component.

Evaluate return in the context of the full policy — not as a standalone ranking.

Status

The status field shows whether a policy is currently available for acquisition.

This matters because resale insurance policies are specific, existing policies. Unlike new insurance plans that can be issued to multiple buyers, each listing represents one actual policy. Once a buyer takes it up, that same policy is no longer available to others.

A policy may be marked as available, newly listed, reserved, or otherwise updated depending on its current position. Always check the status before spending time reviewing a policy in detail — there is no point going through a full document review if the policy is already taken.

If a policy you are interested in has been reserved, contact MAXX CAPITAL to enquire about similar available policies or to be notified when new listings are added.

How to Compare Policies Correctly

When comparing multiple listings, it is tempting to sort by estimated return and start with the highest. That is a reasonable first filter — but only a first filter.

A more complete comparison works through these questions in order:

- Does the initial investment fit my available capital?

- Are there yearly premiums, and can I comfortably maintain them?

- Does the maturity date fit my time horizon?

- What is the projected maturity value, and how much of it is guaranteed?

- Does the estimated return make sense relative to total costs and the remaining term?

- Have I downloaded and reviewed the policy document?

Only after working through these questions does a policy become a properly assessed candidate — not just an attractive row in a table.

Common Mistakes to Avoid

Reading it like a fixed deposit table

A fixed deposit comparison is relatively straightforward — deposit amount, interest rate, and tenure. A resale insurance policy listing looks similar but is not. The underlying asset is a real insurance policy with its own terms, premium obligations, projected assumptions, and ownership transfer process. Treating the two as equivalent leads to under-informed decisions.

Choosing based on return alone

The highest estimated return on the list is not automatically the best policy. A high projected return may reflect a long remaining term, substantial future premiums, or a high dependence on non-guaranteed bonuses. Evaluate return in the context of the complete picture.

Overlooking future premiums

If yearly premiums remain payable, they are part of your total commitment — not a footnote. A policy that looks affordable based on initial investment may require significantly more capital before maturity. Always calculate the total outlay, not just the upfront cost.

Treating projected values as guaranteed

The projected maturity value may include non-guaranteed components. If the actual payout differs from the projection, your actual return will too. Understand the guaranteed versus non-guaranteed split before committing.

Ignoring the policy document

The listing summarises. The document explains. Before investing, always download and read the actual policy document. The table tells you which policies deserve attention; the document tells you whether a specific policy is actually suitable for you.

Not checking availability status

Because each listing is a specific policy, availability changes. A policy that is listed today may be reserved tomorrow. Always confirm status before beginning a detailed review.

Questions to Ask Before Choosing a Policy

Run through this checklist before making any decision:

- Does the initial investment fit my available capital?

- Are there yearly premiums, and am I comfortable paying them through to completion?

- Does the maturity date fit my financial timeline?

- Have I reviewed the projected maturity value and understood the guaranteed versus non-guaranteed split?

- Does the estimated return make sense given my total cost and time commitment?

- Have I downloaded and read the policy document?

- Is the policy still showing as available?

- Have I asked MAXX CAPITAL to clarify anything I am uncertain about?

These questions do not need to be answered in one sitting. They are a review framework — designed to ensure you are choosing a policy based on a complete understanding, not a single appealing number.

How MAXX CAPITAL's Policy List Is Designed to Help

The MAXX CAPITAL policy list is designed to make available resale insurance policies easier to compare and review.

Each listing presents the key figures — policy number, initial investment, yearly premium, projected maturity value, maturity date, estimated return, and status — in a structured format. Each listing also includes a downloadable policy document, so investors can move from a broad comparison to a specific, document-level review before making any decision.

The goal is transparency and clarity at every step.

If you have questions about any listing, or if you would like to understand a policy in more detail before deciding, speak with MAXX CAPITAL. You can also learn more about how investing with MAXX CAPITAL works before taking the next step.